|

1031 Financial Exchange www.1031FEC.com 1031 1033 1045 721 Exchanges Exchange & Asset Tax Consultants |

Matching Clients with Premium Income Investments of Agriculture, Commercial & Energy Properties for 1031 Exchange and Direct Purchase |

1031FEC Your tax solution Advisors

We appreciate your business.

453 721 1031 1032 1033 1034 (Repealed) 1035 Exchanges

121 Exclusion (Replaced 1034)

|

For a Free Cnsultation, Contact us, or Call 800.333.0801 or 941.363.1375

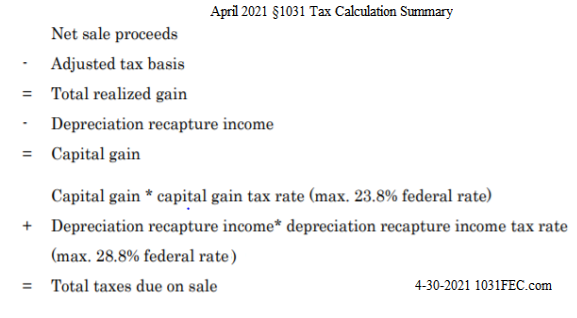

Tax Reduction Services IRS (Internal Revenue Service) IRC (Internal Revenue Code) §1031, and §1033 real property exchanges and stock exchanges remain popular for tax-deferral. If needed two to eight owners of single property can allow owners to purchase larger more secure leased real estate. 1031FEC April 2021 §1031 Tax Calculation Summary

§1031

Tenant in Common is a form of holding title to real property. It allows the owner/owners to own an undivided fractional interest in the entire property. In addition, it has become the preferred investment vehicle for real property investors who wish to defer capital gains via a §1031 exchange and own real property without the management headaches. Most of 1031FEC replacement properties are zero debt with less than 10 owners. The 1031FEC occasional debt TIC has less than 10 TIC owners. The following factors have increased the popularity of Tenant-in-Common (TIC) investments:

In a 1031FEC Premium Tenants-in-Common (TIC) investment you are a co-owner of an entire property. You title as an owner in an undivided interest in the property along with other investors. For example, as a TIC investor in a multi-tenant office, you share in the ownership of the entire property, not a specific office space. Likewise, if you invest in an apartment complex, you share in the ownership of the entire property, not a specific unit. IRS § Section 1032 advantages exchange of stock for property with no gain or loss recognized to a corporation on the receipt of money or other property in exchange for stock (including treasury stock) of such corporation. No gain or loss shall be recognized by a corporation with respect to any lapse or acquisition of an option, or with respect to a securities futures contract (as defined in section 1234B), to buy or sell its stock (including treasury stock). For basis of property acquired by a corporation in certain exchanges for its stock, see your tax advisor, your Qualified Intermediary and 1031FEC. •

IRS § 1031

and §721 TIC

Reduce risk by identifying 1031FEC Premium TIC replacement property for your 1031 Exchange. Identify multiple TIC Properties. Or, acquire interest in multiple TIC Properties. One may directly acquire TIC or most properties without an exchange.

• •If you do replace with one whole property and have proceeds left, you can put these remaining proceeds into the TIC property identified. •Failure to close under 1031 time limit is the #1 reason clients reveal as to why many sellers pay capital gain taxes!

This is an open investment

program. This means that the properties are already purchased and the

investment program structure is in place, eliminating the risk of time

and uncertainty in identifying a replacement property.

The TIC structure has various features that make it attractive to the real estate buyer. Access to Preferred High Grade Properties from Reputable National Real Estate Companies - The typical investment in whole commercial building begins at $1 million, but through premium TIC ownership, the average person is able to enjoy ownership in an institutional-type property with a minimum investment. Besides reliable income and growth potential, these high quality properties are able to attract tenants with greater financial strength and stability than possible for the individual landlord. Combined Real Estate Experience - As an alternative to sole ownership of real estate, a 1031 buyer can take ownership in a large preferred commercial property along with other unrelated buyers, not as limited partners, but as individual owners. Each of the TIC owners brings their previous real estate knowledge to the group. Thus, each decision of the TIC ownership will be backed by many years of real estate experience. Lessee Management with up to 25 Years Experience in Real Estate - Most of the day-to-day property operations are handled by a Master Lessee. The lessee managers control or has involvement in more than $350 million in real estate assets and have extensive experience in real estate. Thus, situations that arise in day-to-day operations will be addressed quickly and efficiently, and the Premium Property TIC owner will enjoy the freedom from property management. Simple Mailbox Management - The Premium TIC property owner avoids the time and frustration of dealing with multiple tenants. You no longer deal with "toilets, tenants and trash," and simply receive your monthly lease payment from your mailbox. Enjoy other interests, travel and time with family. Exact Dollar Matching - In a Premium TIC property, you may be permitted to purchase any amount above the minimum. For example, if you have $152,479 of equity from the sale of a previous property you can purchase $152,479 of equity in a TIC property. Low Minimums - Revenue Procedure 2002-22 issued by the IRS allows up to 35 TIC owners in any one property. Most TIC owners number 15-25 per property. Minimum purchase requirements are structured to meet this limitation and can range as low as $50,000 equity. Non-recourse Financing - The mortgages on most of the Premium TIC properties offered are non-recourse. The TIC debt structure generally allows for the debt financing to assumed. Assumption usually occurs without the need for qualification or loan assumption fees. Diversification - Due to the low minimums in Premium TIC properties, the buyer can decrease risk by diversifying into different properties in various different marketplaces. Speed and Simplicity - Speed and simplicity are achieved due to the efforts of 1031 FEC Consultants, Associates and experienced real estate professionals. The negotiation process is complete, and survey, rent rolls, etc. are already completed and available for your review. After your review of all the due diligence used to acquire your property, and upon your approval, you are ready to close. The closing can be completed in days, not months.

No Closing Costs

- Some property investments include closing costs. Be sure of all costs

in a purchase or exchange. Absent seller default or other items outside the control of

1031 FEC, closings are generally within the agreed upon time frame.

1031 FEC does not charge the TIC owners closing costs.

Non-FEC 1031 triple-net Master Lease transactions generally result in

client closing expenses.

Deeded Interest - The Premium TIC owners buy the property and receive a deeded interest. You can transfer this interest by gift, sale, inheritance, assignment, etc. Such transfer does not need to coincide with the transfer of all TIC interests in the property. If requested to do so by the TIC owner, 1031 FEC will assist in the marketing of any TIC interest. No Special Allocations - All the Premium TIC owners receive lease payments, sale proceeds and the depreciation tax benefits in proportion to their percentage ownership in the property. Impasse Resolution Procedure - On a decision requiring unanimous vote, such as a sale decision, a 75% vote by the TIC owners may be sufficient to initiate the impasse resolution procedure. This procedure allows the TIC owners with 75% or more of the property to make an offer to buyout the dissenting owner with 25% or less of the property. The dissenting TIC owners can either: (1) accept this offer, (2) buy out the 75% TIC owners at the same price per percentage ownership, or (3) change their dissenting vote to a consenting vote.

F As a leader in locating and providing qualified managed premium §1031 Tenants-in-Common (TIC) replacement properties, 1031FEC can offer owners advantages for success. 1031FEC can assist finding the proper 1031 property for your business requirements that can defer capital gains tax and recapture of depreciation taxes. 1031FEC Consultants advise you and your CPA to assist proper IRS documentation and procedure. Reduce stress of management or income collection with 1031FEC TIC and other qualified income properties.

Our

1031FEC Premium TIC Program provides real estate buyers with the monthly rental

income advantage of a triple-net lease with scheduled increases plus single-tenant property with the

appreciation advantages of a multi-tenant property. By owning TIC interests

in premium multi-tenant commercial properties across a wide geographical area, real

estate buyers can enjoy the diversification that is not possible if you were

to buy just one single location property. No Fee to 1031FEC 1031 Exchanger Client. Fee paid by 1031 real estate property provider. See Qualified Managed and Other Premium Investments Featured Real Estate Investment Properties & state locations with minimum investment equity are at Investments. Does your property qualify for this tax break? For a no fee confidential consultation and for more details contact 1031FEC. We also can find if you qualify for a retirement tax deduction up to $100,000 for you and up to $100,000 for your spouse. We recommend your tax advisor or CPA be invited to consult and confirm details. Other 1031FEC Exchange Advantages

Personal Residence to a RentalOne can avoid paying tax on more than $500,000 of gain on one's home. Many people are aware of the advantages of Internal Revenue Code Section 121, which allows a married couple to exclude up to $500,000 of gain on the sale of their personal residence ($250,000 for a single taxpayer). Although this amount of gain is generous in most areas of the country, in some states homeowners receive more than $500,000 of profit when they sell their home. That additional profit is subject to federal and state capital gains tax and net investment income tax (Medicare tax).

What is much less understood in the real estate world is that a homeowner can avoid paying all of the tax on their home by converting it to a rental. Once the home is converted to a rental, the owners can sell it and use both the Section 121 exclusion of gain and the Section 1031 deferral of gain provisions to exclude some of the gain and defer paying tax on the rest. Most tax advisors recommend renting the home for at least two years to establish it as a rental, but if you rent it for too long, you could lose the ability to benefit from the Section 121 exclusion, since that provision requires that you have lived in the home as your primary residence at least two of the past five years.

For example: Bob and Sue Smith have lived in their home for twenty years. They acquired it for $100,000 and it is now worth $1 million, so if sold, they would have $900,000 of gain. If they sell it without converting it to a rental, they would be able to exclude $500,000 of gain but would have to pay capital gains tax on the additional $400,000 of gain.

Bob and Sue decide, however, to convert their property to a rental. After renting it for two years, they sell it for $1 million. Since they used the home as their primary residence at least two of the past five years, they are able to exclude $500,000 of the gain. They can then use the remaining funds to acquire replacement investment property in a 1031 exchange and defer paying tax on the balance of the gain. In order to accomplish this, they must set up the 1031 exchange prior to closing on the sale of the property.

In order to completely defer the remaining gain, the traditional rule is that the investor must acquire replacement property with a fair market value equal to or greater than the relinquished property, and must invest all of the equity from the relinquished property into the replacement property. When gain has been excluded under Section 121, however, the amount of value and equity required to invest in the replacement property is reduced by the amount of gain that was excluded under Section 121.

Homeowners who decide to combine a sale of their primary residence with a 1031 exchange need to comply with all of the rules of Sections 121 and 1031 in order for this to work. Revenue Procedure 2005-14 explains how the two statutes may be combined for one property. This ruling includes not only the situation mentioned above, but also a sale of a personal residence with a home office or separate guest house that is rented.

Some of the requirements to keep in mind are:

Disclaimer: The above brief descriptions are not to be construed as

legal or tax advice and is qualified in its entirety by the actual

closing documents. In case of any discrepancy, the actual closing

documents will control.1031FEC

recommends investors considering an IRS IRC §1031 tax-deferred exchange

transaction or

Email 1031FEC for more information.

Transactions Subject to the U. S. A. Patriot Act Thank you for visiting www.1031FEC.com |

| Home | About Us | For Advisors | 1031 Deferral | TIC | Investments | Roth IRA | My Property | Income | Contact Us | www.1031FEC.com © 2022 |