Ken Wheeler Jr.'s

experience

includes 15 years as a commercial contractor constructing

buildings and agriculture business facilities in the

Midwest. 25 years was as a business broker and financial

advisor including 37 years as a real estate broker involved in assisting business and property owners

to sell, merge or acquire (mergers and acquisitions) and

fund (investment banking). Consistently had challenges to

transfer ownership and maintain wealth. The end goal

challenge generally included an efficient tax and estate

plan. Not a CPA, but work with CPAs and tax attorneys for

asset plan. A CPA and attorney are much like a doctor.

Unless one can tell them where it hurts many can volunteer little. What CPAs,

tax advisors and attorneys tell us is within the scope of their practice that

generally does not work extensively with property transfer tax code.

Experience here is with transferring property and keeping our money,

i.e. saving tax money within the tax code. A CPA/tax advisor

generally knows their client’s tax details best. We can be an assistant to

tax advisors, real estate professionals and a client to minimize taxes when it is a goal.

We do not market

annuities, insurance or list real estate or businesses. We may, with client

request or

permission, refer to those who

do.

Step up Basis at Death - The

Ultimate Death Tax Exclusion Real estate and most

property of value advantage the step up basis

transferring to beneficiaries at current value at death

of owner. In many situations beneficiaries can sell and

owe no tax. Note: Annuities, qualified plans (as IRA,

401k, SEP) and non-qualified (annuities) plans are not

included.

CPA recommended.

****Internal

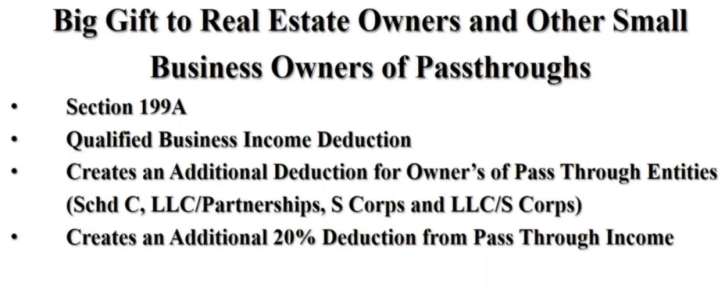

Revenue Code (IRC) §199Aalso known as the “Pass Thru Deduction”

for QSI (Qualified Business Income).There is Now a Deduction for up to 20 Percent of the

Qualified Business Income of Pass Through Entities.

The Act establishes a new deduction for owners of pass

through entities that may enable those owners to deduct up to 20 percent

of their qualified business income. This deduction is effective for

taxable years beginning after December 31, 2017, but expires in taxable

years beginning after December 31, 2025.

IRS Safe Harbor rule (Revenue

Procedure 2019-38 PDF ), CPA recommended.Avoid the

Stealth Tax

See more at

1LessTax or go

HERE

**IRC §121Residence Gain Tax Exclusion

allows two year plus owner

occupancy of residence a $250,000 gain exclusion. If

married spouse can add another $250,000 exclusion

for maximum $500,000 gain exclusion. Over

the $250k/$500k gain exclusion may consider the Energy

Rehab Acquisition or Exchange as an IRC

§1031 replacement property

to tax defer balance of gain.

CPA recommended.

IRC §1031

Tax Deferred Exchange Updated as of

2018, relinquished real property (real estate) only. IRC§1245 (personal property) now not exchanged. Exchange

Accommodator/Intermediary is necessary. Guided by time

limit, replacement property & other significant rules.

CPA recommended.Avoid the

Stealth Taxwww.1031FEC.com

IRC§1033 Tax Deferred Exchange

is for Government

acquisition of real estate by eminent domain. Exchange

Accommodator/Intermediary is not necessary. Guided by

two year time limit and other significant rules. CPA is recommended.

www.1031FEC.com

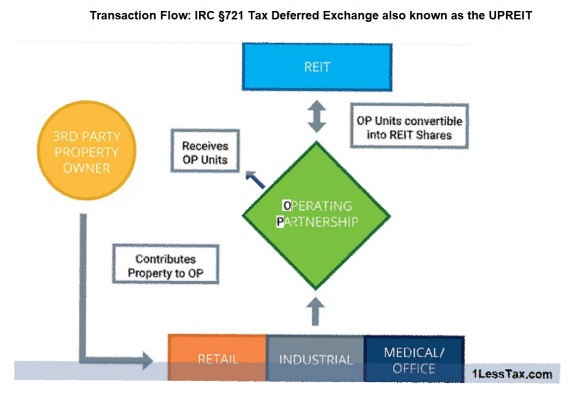

IRC§721 Tax Deferred Exchange also known as the UPREIT. For

an Real Estate Investment Trust acquisition, one

§1031 exchanges into a qualified replacement property

owned by a REIT then into the REIT in an unspecified time. The transfer

into the REIT converts to REIT shares that may be sold

in partial with deferred tax due.

CPA recommended.

IRC §1045

Qualified Business Stock Exchange(aka business

§1031 but better)Qualified Business

is key. Exchange

stock or into qualified business stock. Business

must qualify, is not publicly traded, is not a finance,

real estate, bank, hotel, restaurant, medical with

doctors, attorney or insurance company. Can be an

affiliated service business. Manufacturers,

distributors, retail and service companies are popular

candidates when owned over six months from date business or part of

business acquired. Specialized Attorney and CPA

recommended. Bloomberg

Article

American

Bar Association 1202 Article

IRC §179

has been amended to include types of building

improvements.

Ceiling

was increased to $1,000,000 for tax years beginning

after 2017, with the phase-out beginning at $2,500,000

of qualifying assets placed in service. Avoid the Stealth Tax.CPA recommended.

See more

at 1LessTax

*IRC

§1245 & §179

new or rehab special

building acquisition Generally Agriculture,horticulture and other

single purpose buildings. (advantageous tax code opportunity for any

property including ordinary income) IRC §179 (§168)

new/used equipmentPotential 100% immediate

deduction of any proceeds. CPA recommended.

www.PayNoTax.biz

IRC§469

Managed Passive

Investment Tax Exclusion - Energy Rehab Acquisition

(an advantageous tax code for

including ordinary and all incomes). 100% deduction for deferral. Potential 90% immediate deduction of any

proceeds. Potential IRC §1031

sale tax deferred to qualified replacement property. CPA recommended.Avoid the Stealth Tax.www.PayNoTax.biz

IRC§453

Installment Contract Sale(for some property one can delay paying capital gains,

not always depreciation recapture tax) over a period

of time (deferral). Any amount acceptable as efficient to parties. Attorney and CPA

recommended.

IRC§453TDCO contract for most

property and businessses; reinvest in all assets or keep proceeds.

Depreciation recapture is a

challenge. $1M+ minimum gain or acceptable proceeds to

owner. Tax Deferred,

Cash Out. Energy rehab for potential recapture tax

deferral. Specialized Tax

Attorney & CPA recommended.

IRC

§1202 QSBS Qualified Business Stock Sale Creating Small Business

Jobs Act of 2010 (improving 1993 Act) increased the gain exclusion to 100% of

the total gain for all QSBS issued after September 27,

2010. Each investor $10M or 10 times the aggregate adjusted QSBS

limit. Two million corporations. Some qualify. Combine

with QOZ? Trusts? Estate Plan? Specialized Attorney & CPA

recommended. American

Bar Association 1202 Article

Bloomberg

Article

ABA 1202

Sales Proceeds

Trust SPT Monetized IRC

§453

Contract Sale requires

third party trustee-for most property. Must reinvest in

business investment (the goal is to place proceeds into

insurance securities products continuing inflexibility). Depreciation recapture

is a challenge. $1M+ or acceptable to

owner. Specialized Tax Attorney & CPA recommended.

KW does not

recommend.

Deferred Sales

Trust (Legacy Plan Contract)

DSTSimilar to above.Proceeds to a

managed trust paid out over time. Included in estate.

Avoid probate for all property-assets. Prevent

beneficiary conflict or heirs challenged at handling

money. Specialized Tax Attorney & CPA recommended.

KW does not

recommendunless insured as

Legacy Plan Contract.

See

www.LegacyChange.com

Health Savings Account (HSA)

Better than an IRA? Medical, dental, vision care are

deductible before taxation.

Maximum

contribution is up $50 to $3,550 for individuals and

$100 to $7,100 for families. Maximum catch-up

contributions for people over age 55 remain at $1,000. Health

account options: HSA (Health

Savings Account); FSA (Flexible Spending

Account/Arrangement); HRA (Health Reimbursement

Arrangement).

HSAsare

tied to high-deductible health plans (HDHP). HDHPs are

defined as those plans that have a minimum deductible of

$1,350 for individuals or $2,700 for a family.

Avoid the

Stealth Tax. www.PayNoTax.biz

&

www.LegacyChange.com

Individual Retirement Account (IRA-ROTH IRA,

SEP, Individual (Solo) 401k-ROTH 401k,

Solo or full Defined

Benefit & more) Move Qualified Retirement

Plan into real and personal property.

Learn

how to enhance most highly taxed and popular supposedly tax deferred

and conservative savings products with tax reduction.

(Energy

rehab deferral and §1031 tax deferral has death

step-up valuation and estate asset advantages). Stretch

IRA gone. Misses the death tax

exclusion.CPA recommended.

Avoid Stealth Taxwww.PayNoTax.biz

&

www.LegacyChange.com

Non-Qualified

Retirement Accounts

Includes

various

annuities and variable annuities for tax deferral

ranging from low risk to extremely high risk tax

deferred plans. Highly taxed at any

transfer including death.

Misses the death tax

exclusion.Avoid Stealth TaxWe do not market insurance

or annuities. CPA recommended.

www.PayNoTax.biz

&

www.LegacyChange.com

LegacyChangeIRC§453

+ More IRS Code for Immediate Tax Deduction.

AKA

Grace Income Plans for insured Income

shifting.

Insured guaranteed

income LegacyChange Plan. Immediate tax

deduction relief with insured income stream. Change illiquid assets as land to income.

Partial gifts to your favorite causes.

Avoid probate for all property-assets. Prevent

beneficiary conflict or heirs challenged at handling

money. Replacement as an economical,

simplified Charitable Trust

or Deferred Sales Trust

but with insured guaranteed

income. Generally for property-asset holders $100k-$20M+/-.

LegacyChange Plan Basics

Grace

or charitable

bargain sale with installment contract (reinsured).

LegacyChange Plan acquires asset (by option contract)

LegacyChange Plan divests (sells)

with

non-profit tax advantages.

LegacyChange Plan pays seller with an insured income

installment contract.

Split

interest transaction (multiple interest beneficiaries

for non-profit)

Tax Deed*** with

IRS

Gifting Code Tax

deed at

auction can legally

transfer ownership to the buyer of a property that has been sold due to

delinquent taxes. In a tax

deed sale,

the property itself is sold. Unwanted property can be

valuated and gifted for tax deduction.

CPA recommended.

Avoid the

Stealth Tax.

See more at

1LessTax

Opportunity Zones

QOZ

New program allow one to

defer, reduce and eliminate capital gains taxes. Invests

in areas where locations are deemed challenged for

business growth. May be in a fund. 10 years to maximize

deferral. Combine with 1202? Estate plans? Trusts? CPA recommended.

Revocable Trust

with Pour Over Will 2/3 of us have no will or plan.

Financial Power of Attorney, Health or Living Will

verses will or no will. With will. you, probate and

government jave estate control, or out of control time and

expense. Testamentary trust inside of will? Stirpes

verses per capita? POA, Living Will? LLC, C Corp,

S Corp, Life estate, land trust advantages, popular

titling errors. Attorney & CPA

recommended. PPL-LS?

Combine with?....

Irrevocable

Pure Grantor Trust as a

revocable living trust, you are the creator (grantor)

and the person in control of the property (trustee). One

is a lifetime beneficiary to income only or living in a

trust property. Other people one names, are lifetime

beneficiaries of the assets plus are usually death

beneficiaries.

Anything one transfers

into the trust is immediately protected from creditors

and predators. After five years,

trust assets are invisible to Medicaid.

Assets at your death are included in your

estate. Your beneficiaries receive stepped-up cost

basis.

Estate attorney recommended.

Life Insurance

Irrevocable Trust Bypass estate tax limits tax

free to fund estate tax owed

over Federal

or state limits or other goal. Experienced Attorney and

CPA recommended. www.LegacyChange.com

Eternal or Perpetual Trust, Self-insurance,

Real Estate Easement Plans with

Advanced Tax-Estate Planning.

Irrevocable. For Affluent, Married $23.16M,

Individual $11.58M or as acceptable to owner. Specialized Estate/Tax Attorney

& CPA

recommended.

www.EternalLegacyTrust.com

Avoid the

Stealth Tax!

Have proper Tiltling!

Be aware of Death Tax Exclusion

*Note: An IRC

§1245 "storage facility" differs from a

non-Section

§1245 building in that the latter may contain a work area in

addition to its storage function and may reasonably be adapted to other

uses. Qualifying

§1245 structures cannot contain work areas

except as necessary to care for the livestock, plants or their produce

or to maintain the structure and equipment. For example, having a cash

register inside a greenhouse for handling sales to the public would

disqualify the structure as a

§1245 single purpose structure.

**Note: IRC

§121

$250k/$500k gain exclusion may choose to use the Energy

rehab exchange or acquisition for the balance of the gain.

By the end of 2019, over $15 trillion worth

of inheritance will pass through the probate courts in America. The #1

asset sold first is the real estate. We inform and can assist for

efficient transfer of asset ownership.

Currently

three trillion $

in annuities in USA. 95% are left to heirs. Gain is taxed ordinary

income (now 37% top bracket) plus any state/city tax. Spouse is not

excluded so is taxed at one's death or transfer. Consider energy rehab acquisition.

Your personal

and business CPA/Tax Adviser is always

recommended for your primary tax consultant.

Recommend an

experienced tax and legal advisor who can know you and your

specific situation, local to your property area and

jurisdiction. If one does not have a personal business legal

adviser we can recommend attorneys in all 50 States.

Other common business considerations

could include inexpensive comprehensive liability insurance umbrella and

other life and disability protection.

Senior Delights

2020 rules push retirees into

higher tax brackets, resulting in many having 85% of their

Social Security benefits taxed as well as many being

penalized by tax for higher Medicare premiums.

Deduction of Medicare Premiums for the Self-Employed;

Folks who continue to run their own

businesses after qualifying for Medicare can deduct the

premiums they pay for Medicare Part B and Part D, plus the

cost of supplemental Medicare (medigap) policies or the cost

of a Medicare Advantage plan.

This deduction is available whether or not you itemize and

is not subject to the 10% of AGI test that applies to

itemized medical expenses. One caveat: You can't claim this

deduction for premiums paid for any month that you were

eligible to be covered under an employer-subsidized health

plan offered by either your employer (if you have a job as

well as your business) or your spouse's employer (if he or

she has a job that offers family medical coverage).

A College Credit for Those Long Out of College;

College credits aren't just for

youngsters, nor are they limited to just the first four

years of college. The Lifetime Learning credit can be

claimed for any number of years and can be used to offset

the cost of higher education for yourself or your spouse . .

. not just for your children.

The credit is worth up to $2,000 a year, based on

20% of up to $10,000 you spend for post-high-school courses

that lead to new or improved job skills. Classes you take

even in retirement at a vocational school or community

college can count. If you brushed up on skills in 2019, this

credit can help pay the bills. The right to claim this

tax-saver phases out as income rises from $58,000 to $68,000

on an individual return and from $116,000 to $136,000 for

couples filing jointly.

Social Security Tax; if you're self-employed and

have to pay the full 15.3% tax yourself (instead of

splitting it 50-50 with an employer), you do get to write

off half of what you pay. Plus, you don't have to itemize to

take advantage of this deduction.

General Business

Operating Procedure

When someone asks for personal information of any kind

please keep in mind you can ask the same of the person or

entity who is asking you, and should do so. Why would one do

business with an unknown?

Have you had people ask for your financial statement?

Ask for their current financial statement.

Especially when anyone is asking for your funds or any

business transaction that could affect your funds, this

should be a common response by you along plus ask for

references from past business clients and associates. Then

one checks the references that have a known legitimate

presence.

Otherwise, it is as purchasing anything without proof of

title or proven position from an unknown person or entity.

After business people are proven legitimate and doing

business in a proper and legal manner, then there is the

normal risk of doing business.

If anyone does not wish to prove their qualifying business

existence that is the first big flag to move on.

Recommend one purchase a subscription to a background

checking service. There are many online.

For one who qualifies with real property real estate we have

replacement properties for 1031 tax deferral. Some are rehab

commercial property. Some are new 15-20-year absolute leased

high-end income properties leased to tenants with positive inflation

and recession resistance. This is accomplished by location and type

of business.

Rehab

(rehabilitated, improved or reworked properties generally have the

option or plan to divest within two-three years rolling into another

wealth building property. They may or may not have an option for

deferred income.

The energy

rehab properties are with known management and rework operators. As

with any venture recommend new associates have references for

experience and integrity. For energy rehab my choice is a CPA firm

that has a business end with consulting and actual rehab projects

they manage. Former Deloitte CPAs, they have decades experience in

oil & gas operations and taxation. This can be the resource for

clients and CPAs to advantage the most prolific tax advantages in

the US tax code. Their experience includes years of alternatives to

be tax efficient.

The energy

rehab property minimum entry income properties are $100k and more. The property

is producing oil & gas. The goal is to buy low, improve the production

and income rolling into another or 1031 out to different qualified

property. One receives recorded ownership document allowing

divesture when desired with a two-three divest year goal. There can

be sheltered income options. Each associate has their personal tax

plan and goals. One can build with one’s own tax protected annuity

with periodical tax-deductible contributions. Up to $5M or more of

acquiring an energy rehab property one potentially deducts 100% of

any income, gain, depreciation recapture, investment or ordinary,

personal, real estate or business asset proceeds with a 15 year loss

carry forward.

We include a

non-disclosure confidentiality document for doing business. We are

searching for long term integrity associates with common goals.

Look forward to knowing you and your goals.

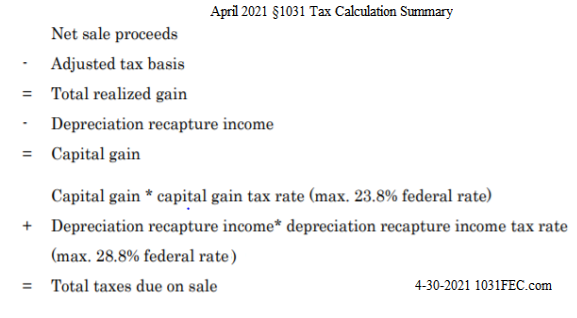

1LessTax.com – Ken Wheeler Jr. Sample Tax Scenario

Avoid

the Stealth Tax.

Funding of property or

asset (BASIS): $200,000.00

Divest or sell

for: $300,000.00

Gain or

Profit $100,000.00

TAXABLE

$100,000.00

For an

energy rehab $100,000.00 is the prime amount to deduct so is the

first amount to consider to transfer to the energy rehab property.

One does

not have to transfer the complete amount as in a 1031 qualified

exchange or other defer/deduct methods.

The

energy rehab property is real property so when one divests one can

choose any other business property to defer tax with the 1031 rule

or refund into another energy rehab property with or without basis,

deducting all.

With the

right people one can have as an energy property annuity to receive

and deduct most income and proceeds from any transaction.

Income for which services have been performed. This includes

wages, tips, salaries, commissions, and income from

businesses in which there is material participation.

Passive Income

Most types of passive income are derived from real

estate/property, while other types of passive income are

derived from royalties from patents or license agreements.

An income stream falling into this category is one where

money is received usually on a regular basis, where no

additional effort has taken place. Most passive income

streams require great effort to start with.

Some examples: Interest Income paid from bank deposits,

rental income from real estate/property., royalties from

writing a book, dividends from shares holding.

Another example of passive income come from network

marketing.’

Passive income flows to you or your family whether you are

sick, or vacationing, or dead. Passive income streams allow

you to make money without having to be there.

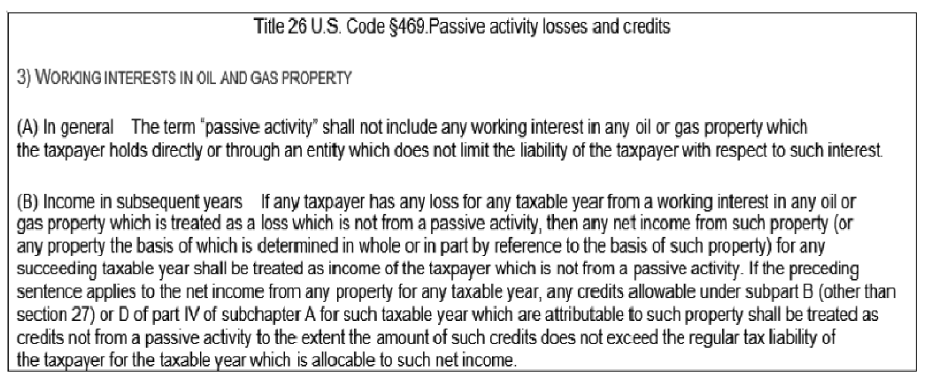

Note:

§469 only exception below.

Portfolio Income

Portfolio income is income from investments, including

dividends, interest, royalties, and capital gains. I would

say that portfolio income is a subset of passive income.

Many owners wish to sell from management intensive

property to fully managed and less risk foundation income property that is

held for the step up basis allowing beneficiaries to sell with no tax.

Note to owners of real estate in different states may

have estate and /or income tax

for property in a state other than the state of residence

that may have no estate (inheritance) tax or state income tax. DST

investments owned by an out of state owner hopefully are located in states

without estate tax and gain tax capture or owner in for a surprise.

The U.S. states that collect an inheritance tax as of 2020 are Iowa, Kentucky, Maryland, Nebraska, New

Jersey,

and Pennsylvania.

Each has its own laws dictating who is exempt from the tax, who will have to

pay it, and how much they'll have to pay.

****IRC Section

§199A aka the “Pass Thru Deduction”

There is Now a Deduction for up to 20 Percent of the

Qualified Business Income of Pass Through Entities

The Act establishes a new deduction for owners of pass

through entities that may enable those owners to deduct up to 20 percent

of their qualified business income. This deduction is effective for

taxable years beginning after December 31, 2017, but expires in taxable

years beginning after December 31, 2025.

The special Code Sec.

§199A deduction is available not

only for individuals but also for trusts and estates. In combination

with the reduction in individual income tax rates, taxpayers eligible to

claim the full 20 percent deduction will face an effective maximum

marginal federal income tax rate of 29.6 percent (plus, the Medicare tax

on unearned income, to the extent applicable) on their eligible pass

through entity income.

In calculating qualified business income, capital gain

income is excluded. As a result, no material deduction would be

available to a taxpayer owning rental real estate if there is little or

no net income generated over the property’s holding period and the only

material income is the gain recognized on the disposition of the

property.

IRC (Code Section)

§179 was amended to make the following types of building

improvements

These building improvements are

not normally within the definition of qualified

improvement property because they are a structural

component of a building — eligible for Code

§179

expensing: (i) roofs, (ii) heating, ventilation, and

air-conditioning systems, (iii) fire protection and

alarm systems, and (iv) security systems. The Code

§179 ceiling was increased to $1,000,000 for tax

years beginning after 2017, with the phase-out

beginning at $2,500,000 of qualifying assets placed

in service.

It is always time to remember important year-end planning.

One has to take action before year-end if one wishes the "de minimis safe

harbor election" (one probably wants it)

in place for 2020 to "expense" assets costing $2,500

or less.

The following are four benefits of this safe harbor:

1.Safe harbor expensing is superior to

§179 expensing because you don’t have "recapture"

(i.e. - the need to "pay back" the expense if you

stop using the asset).

2.Safe harbor expensing takes depreciation out

of the equation.

3.Safe harbor expensing simplifies your tax and

business records because you don’t have the assets

cluttering your books.

4.The safe harbor does not reduce your overall

ceiling on Section 179 expensing.

Safe harbor example: One has a

small business that elects the $2,500 ceiling for

safe harbor expensing and purchases two desks costing

$2,100 each. The invoice states the quantity

“two” at the total cost of $4,200, plus sales tax

of $378 and a $200 delivery and setup charge,

totaling $4,778.

Before this safe harbor, one would have capitalized

each desk at $2,389 ($4,778 ÷ 2) and then either

Section 179 expensed or depreciated it. You would

have maintained the desks in the depreciation schedules

until disposed.

With the safe harbor, one expenses the

desks as office supplies. This makes the tax event easier.

To benefit from the safe harbor, one and tax

preparer do a two-step process as this:

Step 1.

For safe harbor protection, one must have in place

an accounting policy—at the beginning of the tax

year—that requires expensing of an amount of your

choosing, up to the $2,500 or $5,000 limit.

Step 2.

When preparing your tax return, one chooses the

election on your tax return to use safe harbor

expensing. This requires attaching the election

statement to your federal tax return filing the tax return by the due date (including extensions).

If one wishes to use this safe harbor for next year,

Step 1

needs to be completed in the current year.

***Tax Deed Purchase

Can Have Tax Advantage When Property Owned Deemed Unwanted

A tax

deed can legally

transfer ownership to the buyer of a property that has been sold due to

delinquent taxes.

... In a tax

deed sale,

the property itself is sold. The sale which

occurs through an auction has a minimum bid of the amount of back taxes owed

plus interest, as well as costs associated with selling the property.

The highest bidder now has the right to collect the liens, plus

interest, from the homeowner. If the homeowner can't pay the liens, the

new lien owner can foreclose on the property. In a tax

deed sale,

a property with unpaid taxes is

sold in its entirety, at auction.

When you

buy a tax lien

certificate, you're buying the

right to receive a debt payment, not the deed to the house.

The homeowner is still the legal owner of the home. If he does not pay the tax debt,

then you

can foreclose.

But you cannot buy a tax lien,

turn around and foreclose on the property the

next day.

Tax Liens do not eliminate the mortgage(s)

attached to the property.

Tax Sales do not remove Assessment

or IRS Liens (government liens), if they are attached to the property.

Investors buy

the liens in

an auction, paying the amount of taxes owed

in return for the right to collect back that money plus an interest

payment from the property owner. ... Ownership of the property rarely happens: The taxes are

generally paid before the redemption date. The interest rates make tax

liens an

attractive investment.

When tax deed purchase lead to clear deed ownership, property can have

development advantages. Environmental situations are to be considered if

only land or land with improvements.

If one wishes to have a professional valuation of an owned deed from a

tax sale, the valuation could be valuable if one contributes the deed to

a charity, government or entity who will accept title. The valuation could be much

more than the purchase and valuation expense allowing a tax deduction for the

contributed valuation.

An installment sale is a sale of eligible property where one

receives at least one payment after the close of the taxable

year in which the sale occurs.

If

one has a profit on an installment sale, one reports part of

your profit when one receives each payment.

One

documents the buyer’s obligation to make future payments, with a

deed of trust, note, land contract, mortgage, or other evidence

of the buyer’s

debt. One should secure the debt.

Although one can’t use the installment method to report a loss,

one can choose to report all of your gain in the year of sale.

Installment

Sale Advantages

An

installment sale offers a number of advantages for you as a

seller, as well as for your buyer:

1.

One can negotiate the sale without the need for the buyer

to pay the full sale price when one finalizes the sale.

2.

One can finalize the sale agreement without waiting for the

buyer to qualify for third-party financing.

3.

One can tailor the terms of the sale to meet needs without

having to get approval from a third-party lender.

4.

One can defer taxes on gain, and potentially pay a lower

tax rate in a later year.

5.

The buyer receives full basis in the property.

How

Is an Installment Sale Reported?

Payments

that received from an installment sale consist of three parts:

1.

Interest

2.

Taxable part (gain or profit)

3.

Non-taxable part (return of basis)

Each

year one receives a payment, one pays taxes on the interest and

taxable part. The part of the payment allocated to your basis is

ot taxable.

Basis

is the amount of your investment in the property for installment

sale purposes.

After

one determines how much of each payment to treat as interest,

one next determines the taxable portion of the remaining

payment.

No Installment Sale in These Instances

There

are certain types of property and transactions for which the

installment method cannot be used, such as:

The sale of inventory consisting of personal property. But this

rule does not apply to property used or produced in farming.

The sale of real property held for sale to customers in the

ordinary course of a trade or business.

Dealers of timeshares & residential lots can treat certain

sales as installment sales & report under the installment method

if they elect to pay a special interest charge.

·The

sale of stock or securities traded on an established securities

market.

·The

sale of depreciable property to a related buyer, unless you can

show to the satisfaction of the IRS that the sale was not made

for tax avoidance.

Tax Reduction To Enhance Annuity, IRA and 401k Ownership

For IRA, 401k, annuity

and other retirement plan owners.

Most plan owners do not

realize retirement plan and annuity ownership transfer is subject to the highest

Federal and state tax rates. Annuity taxation is immediate

unless in qualified plans. Learn

how to enhance most highly taxed and popular supposedly tax

deferred and conservative savings products with IRS tax codes for

tax reduction.

Maintain the tax deferral plus add tax deductibility, as a LegacyChange plan and other

available tax advantages

to this conservative savings instrument.

We do not market or sell

annuities or insurance products. Our goal is to assist to

significantly reduce the massive

taxation of these assets.

Contact us

Avoid the Stealth Tax

ANNUITIES

How Long Will Payments Last?

A major consideration is

if one wishes risking losing a

significant portion of your investment to the annuity company if you

die before receiving enough payments to justify the annuity

purchase. There are options.

These options include:

Single Life/Life Only

Lifetime of payments but no survivor benefit.

Life Annuity with Period Certain (Fixed Period/Guaranteed

Term)

Minimum period of payments - even after death of buyer -

with remaining payments to beneficiary.

Joint and Survivor Annuity

Payments last life of both spouses.

Lump-Sum Payment

Entire annuity paid at once with heavy tax burden.

Systematic Annuity Withdrawal

Amount and frequency of payments customizable.

Early Withdrawal

Withdraw before 59 1/2, pay 10 percent in taxes. 72T

IRA Withdrawal

Rules have minimum required distributions after 72 with

a10 year disbursement requirement for beneficiaries receive

all.

Limitations

Some annuities limit choices.

Single Life/Life Only

Also known as a straight-life annuity, this choice allows you to

receive payments your entire life. Unlike some other options that

allow for beneficiaries or spouses, this annuity is limited to the

lifetime of the annuitant with no survivor benefit. The risk is you

will die before getting all or most of your money back. You can

limit the possible loss here by choosing a life annuity with period

certain.

Life Annuity with Period Certain (Fixed Period/Guaranteed Term)

Period certain annuities are the same as a straight-life annuity,

but it includes a minimum period the payments will last – say 10 or

20 years – even if the annuitant dies. If the annuity holder dies

before the end of the period, the payments for the rest of that time

will go a beneficiary or

the annuitant’s estate. Adding the period certain will cost you,

lowering the amount of your monthly payments.

Joint and Survivor Annuity

Also known as a joint-life annuity, a joint and survivor annuity

guarantees payments will last the lives of both the annuitant and

another person, typically a spouse. This choice reduces the amount

of each payment you receive with a life annuity or a life annuity

with period certain. You can also elect to include a period certain

with a beneficiary receiving payments if both you and your spouse

die before the end of the period.

Lump-Sum Payment

This option allows the annuitant to receive the entire worth of the

annuity at one time. This can increase the tax burden substantially

by requiring taxes all be paid in that year.

Systematic Annuity Withdrawal

In this method, you choose the amount of the payments and how many

payments you want to receive. This option does not include a

guarantee it will last your entire life. It is entirely dependent on

the amount of money in your annuity account.

Early Withdrawal

If you elect to withdraw money from your annuity before you reach

the age of 59 ½, you will have to pay a penalty of 10 percent to the

government, in addition to whatever taxes

you owe on the money. If that withdrawal is within five to seven

years of purchasing the annuity, you may also owe the annuity

provider a surrender charge of as much as 20 percent, depending on

how much time has passed since the purchase.

Death Benefit

Your annuity contract may include a provision for a death benefit

for a beneficiary you designate. Usually, the payout for the

beneficiary will be the contract value or the amount of the premiums

that have been paid.

TIP

If

you are the non-spouse beneficiary or spouse beneficiary of an annuitant who has died,

you have a few different options to receive payment from a

nonqualified, deferred annuity unless the annuitant has arranged

otherwise.

Five Year Rule

One involves invoking a requirement that all the money in the

annuity must be distributed within five years of the annuitant’s

death.

Beneficiary Life Expectancy

The beneficiary may also choose to have the money distributed

according to his or her life expectancy. The life expectancy is used

to calculate the minimum amount the beneficiary must withdraw each

year.

Survivor Annuitization

And finally, the beneficiary may choose to annuitize the funds. This

means the annuity becomes a guaranteed stream of income for the

beneficiary. This can use the single-life or term-certain options

described above.

Do Annuities Have Declared Dividends?

Annuities are different than stocks and do not have the same

structure. With stocks, you have public corporations with boards of

directors that decide to declare a dividend for payments to

shareholders from company profits. Annuity payments are either fixed

ahead of time or tied to the performance of an index or stock

portfolio.

We do not market or sell

annuities or insurance products.

Significantly reduce the massive taxation of these assets.

Avoid the

Stealth Tax.

About Life Insurance Settlement

Contracts

Minimum policy benefit

$500,000 (preferably $1M+) No maximum policy

benefit 60 Years of age + with

impairments 70 Years of age + without impairments

All types of policies Less than

12 Years life expectancy The amount paid into

the policy (the tax basis)

is tax-free.

Proceeds greater than the tax basis,

but less than the cash surrender value, are taxed at

ordinary income rates. Any remaining amount is subject

to capital gains tax. CPA & tax

attorney recommended!

We do not market

annuities, insurance or list real estate or businesses.

We may, with client

request or

permission, refer to those who

do.

What is a 529 Plan?

A 529 Plan is a savings vehicle designed

specifically for higher education expenses. The name “529” comes

from Section 529 of the federal tax code, which authorizes

states to offer the plans. There are two types of 529 Plans –

Prepaid and Savings, and both Prepaid Plans and Savings Plans

are authorized 529 college savings plans. Earnings in 529 Plans

are tax-free when they are used for Qualified

Higher Education Expenses. In general,

qualified expenses include tuition, fees, room and board, and

the cost of books, supplies and equipment required for the

enrollment or attendance at an Eligible

Educational Institution, including

undergraduate, graduate, and vocational/technical schools.

What is the difference between a Prepaid Plan and

a Savings Plan?

A Prepaid Plan is basically a prepackaged college

savings plan covering specified college costs in the future.

Prepaid Plans simplify saving for future college costs. You do

not have to worry about how much to save, when to save or how to

invest with a Prepaid Plan. Simply pick a plan, make your

payments, and when your student is ready for college, the plan

pays for the costs covered by the plan. The Prepaid Plans

offered by the Florida Prepaid College Board are guaranteed by

the State of Florida, so you can never lose what you’ve paid

toward the plan.

A Savings Plan allows you to develop your own

plan to save for college. You decide how much you want to save

and when you want to save. You also get to choose how you want

to invest your savings using the investment options offered by

the plan. When it comes time for college, you use your savings

to pay for actual college costs at that time. Savings Plans are

not guaranteed, so the value of your investment is subject to

market fluctuations.

Can I enroll in both a Prepaid Plan and a Savings

Plan?

Yes. Prepaid and Savings Plans work well

together. For example, you could use a Prepaid Plan to cover up

to four years of tuition and fees and a Savings Plan to pay for

books, a computer, room and board. If you don’t want to use a

Prepaid Plan to save for all four years of tuition and fees, you

could purchase a 2-Year Florida College Plan or one or more

1-Year University Plans and also open a Savings Plan.

When deciding how to save, focus on your

investment preferences. For example, do you prefer guaranteed

investments (Prepaid) or investment control (Savings)?

Also, consider what you can afford. You may want

to, but you don’t have to save for everything. Parent surveys

suggest that most parents anticipate paying 40% of their child’s

higher education expenses.

How does a 529 Plan compare to other college

savings vehicles?

Savings vehicles like 529 Plans offer distinct

advantages over traditional checking or savings accounts, namely

the opportunity for tax-free earnings. Here is how 529 Plans

compare to other college savings vehicles.

529 Plans

Coverdell Education Savings Accounts

Qualifying U.S. Savings Bonds

UGMA/UTMA

Federal Income Tax

Contributions made with after-tax funds;

earnings excluded from income for federal tax

purposes when used for qualified college

expenses

Contributions made with after-tax funds;

earnings excluded from income for federal tax

purposes when used for qualified college and

K-12 expenses

Certain “EE” and “I” bonds may be redeemed

tax-free for college expenses

First $1,050 is tax-exempt; unearned income over

$2,100 for certain children under age 24 is

taxed at parent rate

Federal Gift Tax Treatment

Contributions treated as gifts; annual and 5-yr…

federal exclusions apply

Contributions treated as gifts; annual federal

exclusions apply

Not considered a gift

Contributions treated as gifts; annual federal

exclusions apply

Federal Estate Tax Treatment

Value excluded from contributor’s estate;

included for death during 5-yr.. election period

Value excluded from contributor’s estate

Value included in owner’s estate

Value excluded from contributor’s estate

Maximum Investment

$418,000 per Beneficiary in Florida

$2,000 per Beneficiary per year (all sources)

$10,000 face value per year, per owner, per type

of bond

No limit

Qualified Expenses

Tuition, fees, books, computers and related

equipment, supplies, special needs; room and

board for minimum half-time students

Tuition, fees, books, supplies, equipment,

special needs; room and board for minimum

half-time students; additional categories of

K-12 expenses

Tuition and fees

No restrictions

Change Beneficiary

Yes

(member of family)

Yes

(member of family)

Not applicable

Prohibited

Time/Age Restrictions

Prepaid: Enroll before 11th grade, 10-yr..

benefit period

Savings: None

Contributions before Beneficiary reaches age 18;

use of account by age 30

Bond purchaser must be at least 24 years old at

time of bond issuance

Custodianship terminates when minor becomes

adult

Income Restrictions

None

Contributions limited for incomes approx. $100K

and above

Interest exclusion for incomes approx. $77K and

below

None

Federal Financial Aid

Asset of parent if owner is parent or dependent

student

Asset of parent if owner is parent or dependent

student

Counted as asset of bond owner

Counted as asset of the student

Use for Non-Qualifying Expenses

Withdrawn earnings subject to federal tax and

10% penalty

Withdrawn earnings subject to federal tax and

10% penalty

No penalty; interest on redeemed bonds included

as income

For specific information about your situation and options,

please consult an investment adviser or certified public

accountant.

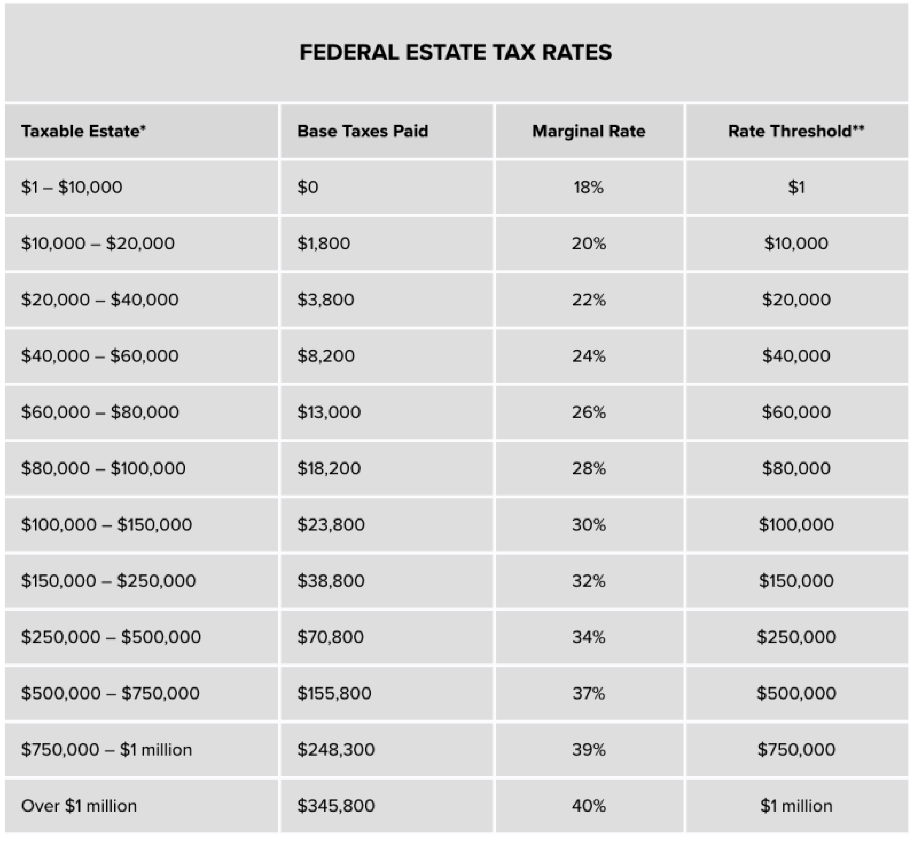

2020

The

estate tax exemption amount is $11,580,000 per person.

Summary outline of six tax methods to

increase efficient affluent client activity

1.IRC

§1202, modified

§1202 and other IRS code

methods to reduce, exclude or defer taxes for ordinary income or

divesting of assets; No Fee until owner has proceeds for tax

success:

1.Tax exclusion & tax deferral entities, $1M+ gain

3.Property owner's CPA

opportunity to be educated and trained in IRS

code for tax reduction, tax exclusion & tax deferral.

IRC

§1202 and Tax Deferred

Cash Out tax exclusion or tax deferral methods considered.

No fee.

4.Property

owner and CPA consider to employ tax attorney service to guide a

transaction to preferred tax reduction goal. No fee.

5.Property

owner and CPA employ tax attorney service to view Letter of Intent or and contract before

parties sign. No fee.

6.Tax

attorney service engaged, have successful closing with tax goals,

owner receives proceeds. Success fee

2.Irrevocable

Trust Management by trust attorney group with approximately 100

billionaires, 300 centimillionaires + many more:

Perpetual

trust

Tax

reduction, no state tax and other tax advantages

Asset legal

protection by trust

Best trust

managers and management policy

Private bank

trust available

Work

fee-based verses valued % fee

No probate

3.Combination

of an Irrevocable Grantor Trust and a Revocable Trust with pour over

will:

1.For anyone owning assets

2.Protect assets from creditors

3.

Control and manage all assets

4.Simpler trust self-management

5.No probate

4.IRC §179

has been amended to include types of equipment

plus building

improvements.

Ceiling

increased to $1,000,000 for tax years beginning

after 2017, with the phase-out beginning at $2,500,000

of qualifying assets placed in service.

Replace IRC §1031.Use

assignment in some cases. CPA recommended.

5.

Legacy plans for economic asset management with guaranteed

income in most states:

Immediate tax deduction-reduction.

Deductions can have five year carry forward

Guaranteed insured income through non-taxable 20 plus year Christian

charity

Simplified, little to no management, defer income or receive monthly

or quarterly income

Your Legacy. Dispense Legacy funds in to the future. Can adjust some terms in future

Little or no attorney expense,

numbers prepared to assist client’s CPA

Eliminates family conflict and executor mismanagement

Ideal

for beneficiaries without money management abilities

No probate - by passes will or

trust

Choose your charity

6. All asset owners;

Immediate tax deduction + asset management + high

income

For 2020 returns, the 0% rate for long-term gains and qualified

dividends applies for taxpayers with taxable income under $40,000 on

single returns and $80,000 on joint returns.

Do you have an entity? This can provide some protection from

liability related to claims against the business.

Have you filed your annual reports?

If you have a corporation, have you had annual meetings of

the shareholders and directors?

Do you have a shareholder agreement/operating agreement

governing the relationship between the owners? This could

address, for example, how, when, and to whom owners can

transfer their ownership interests; how distributions of

cash are made to the owners; and whose approval is required

for certain actions.

Do you have a succession plan for your business? This may tie in

with your estate plan.

Do you know what intellectual property (“IP”) your business has?

This could relate to your name; logo; domain name; website,

social media, or other written content; photographs; or your

product itself.

Have you registered/maintained important IP?

Are you enforcing your trademarks? This can include your

business and product names, logos, and taglines. Trademark

rights may be eroded if these rights are not enforced

against infringers.

Are you maintaining the secrecy of your trade secrets? Do

you have confidentiality agreements with your

employees/contractors?

Do you have an agreement stating that you own IP created by your

employees/contractors?

Do you own your domain name? Sometimes an employee or contractor

may register in their name rather than the business’s.

Does your website have terms of use and a privacy policy?

Are you complying with the Digital Millennium Copyright Act?

This can provide protection if someone posts content on your

website (for example, through a chat room or comment) that

infringes a third party’s copyright.

Are you protecting and securing electronic data that contains

personal information (including information you may collect

through your website)?

Are you using third-party content/likenesses on your website? If

so, you should confirm these are used properly.

The SECURE Act is Tax Heavy Rule Changes for IRA Owners

“The SECURE Act changed a lot of what we believe about

inherited IRAs,” said Rochelle Schultz, an estate planning

lawyer at Weinstock Manion in Los Angeles. “Everyone,” she

added, “needs to bring it up to their estate attorneys or

financial advisors to make sure beneficiaries understand

what’s going to happen.”

The 10-year rule hits retirement accounts inherited from

people who pass away on or after January 1, 2020. Wealth

advisors call the curb the death of the “stretch IRA,”

because an heir can no longer “stretch out” withdrawals from

the account over her lifetime. The change reflected the

Biden administration’s desire to expand retirement options

for Americans while curbing the tax benefits of passing

tax-deferred wealth to heirs.

Five years

IRS rules that pre-date the SECURE Act say that if a

taxpayer dies before beginning required minimum

distributions, typically at age 72, and hasn’t specified who

will inherit their IRA or 401(k), then the account goes into

the deceased’s estate. The estate’s heir or heirs then have

five years to drain the account. The five-year

rule also applies to inherited Roth IRAs in

existence for less than five years. And it applies to some

beneficiaries who inherit a retirement plan through a

so-called beneficiary account, like a trust.

Under prior IRS rules, the beneficiary of a broad type of

estate planning vehicle known as a “see-through” trust is

treated as if she directly inherits the trust’s assets, even

as the vehicle is technically the beneficiary. The IRS

“looks through” the trust to see that an actual human being

— the trust’s beneficiary — is there. Before the 2019 law,

those people could stretch out withdrawals over their

lifetime. Now, depending on whether the trust is properly

set up, the 10-year deadline could be five years.

That's in part because IRS rules for see-through trusts are

strict. Along with record-keeping requirements, the tax

agency requires that the vehicles be irrevocable, valid and

legal in the state where they’re set up and clear about the

identity of its beneficiaries. If a trust doesn't meet those

requirements, beneficiaries can be required to drain them in

five years.

The issue is that the SECURE Act doesn’t spell out whether

its 10-year rule applies to see-through trusts. Nor has the

IRS offered guidance on the issue. If the rule doesn’t

apply, then some beneficiaries of those trusts might have to

empty out an IRA within five years as before — an outflow

that can spike an heir’s income and tax rate.

“There is still ambiguity as to how the rules surrounding

‘see-through’ trusts will apply post-SECURE Act,” wrote Fidelity

Investments earlier this year.

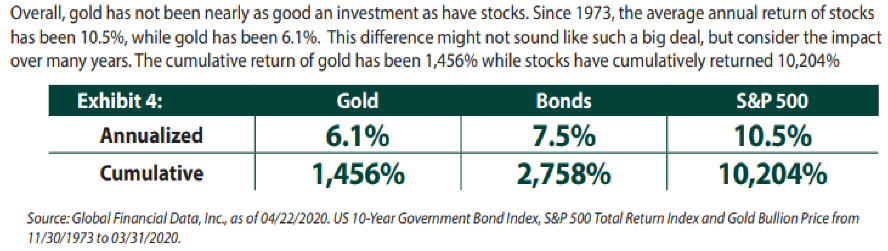

GOLD

verses STOCKS

REAL ESTATE (Business Income)

Residential properties have an average annual return of 10.6

percent, commercial properties have a 9.5 percent average return,

and REITs have an 11.8 percent average return.

Knowing the national average return on an investment property is

extremely useful for comparing your return on investment properties.

The 70% rule helps

home flippers determine the maximum price they should pay for an

investment property.

Basically, they should spend no more than 70% of the home's

after-repair value minus the costs of renovating the property.

The 1% rule of real estate investing measures

the price of the investment property against the gross income it

will generate.

For a potential investment to pass the 1% rule, its monthly rent

must be equal to or no less than 1% of the purchase price

TDCO

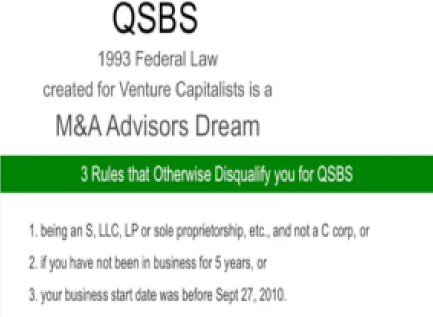

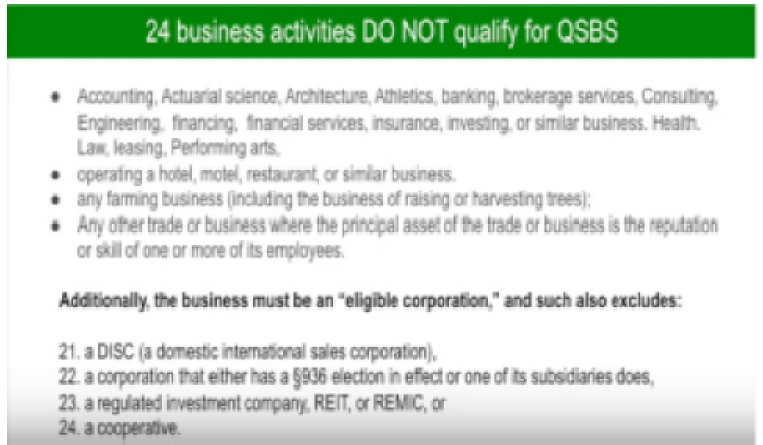

TDCO QSBS

QSBS Rules

Rules