|

|

|

|

|

|

|

|

Tax Efficiency Services - Pay No Tax Alternatives - Definitions - Scenario

When Planning, Transferring, Flipping or Selling Any Property or Business

Summaries of Alternatives For Diversification While Saving Tax Expense

Reduce Tax Burden Protect Taxable Gains Maintain & Increase Wealth Protect Income

|

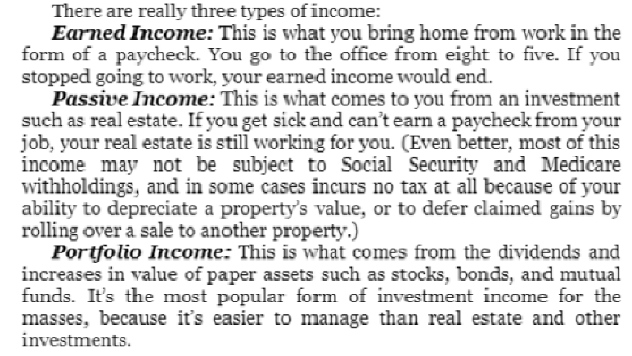

PayNoTax.com – Ken Wheeler Jr. Background includes 15 years as a commercial contractor constructing buildings and agriculture business facilities in the Midwest. 25 years as a business broker and financial advisor involved in assisting business and property owners to sell, merge or acquire (mergers and acquisitions) and fund (investment banking). Consistently had challenges to transfer ownership and maintain wealth. The end goal challenge generally included an efficient tax and estate plan. Not a CPA but worked with CPAs and tax attorneys to plan. A CPA and attorney are much like a doctor. Unless one can tell them where it hurts they generally volunteer little. What CPAs, tax advisors and attorneys tell us is within the scope of their practice that generally does not work extensively with property transfer tax code. Experience here is with transferring property and keeping our money, i.e. saving tax money within the tax code. A CPA/tax advisor generally knows their client’s tax details. We can be an assistant to tax advisors, real estate professionals and a client to minimize taxes when it is a goal. Real Estate & Asset Titling Exit Strategies with Tax Deferral, Deduction & Reduction Can Involve Estate Plan The Final Life Plan with Legacy & Beneficiary Consideration When selling any type assets and properties we have several tax obligation choices.

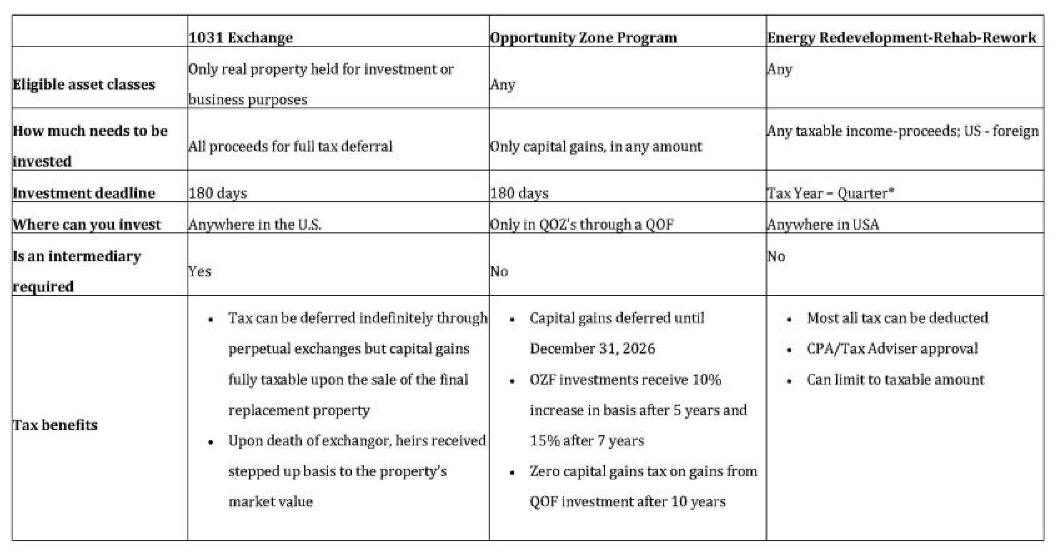

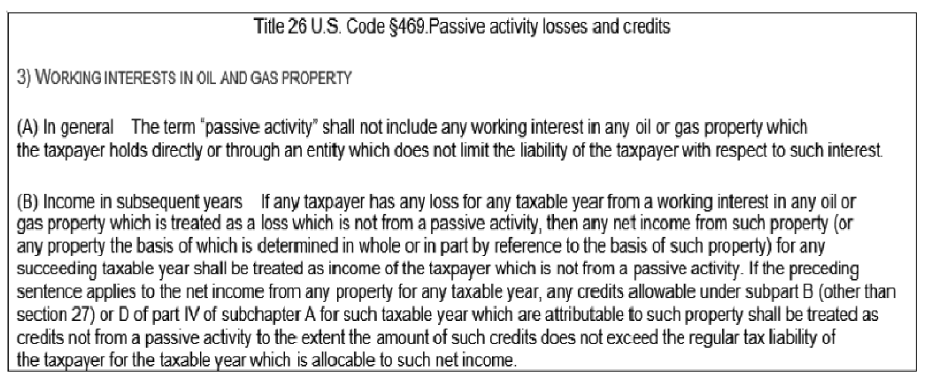

For one who qualifies with real property real estate we have replacement properties for 1031 tax deferral. Some are rehab commercial property. Some are new 15-20-year absolute leased high-end income properties leased to tenants with positive inflation and recession resistance. This is accomplished by location and type of business. Rehab (rehabilitated, improved or reworked properties generally have the option or plan to divest within two-three years rolling into another wealth building property. They may or may not have an option for deferred income. The energy rehab properties are with known management and rework operators. As with any venture recommend new associates have references for experience and integrity. For energy rehab my choice is a CPA firm that has a business end with consulting and actual rehab projects they manage. Former Deloitte CPAs, they have decades experience in oil & gas operations and taxation. This can be the resource for clients and CPAs to advantage the most prolific tax advantages in the US tax code. Their experience includes years of alternatives to be tax efficient. The energy rehab property minimum entry income properties are $100k and more. The property is producing oil & gas. The goal is to buy low, improve the production and income rolling into another or 1031 out to different qualified property. One receives recorded ownership document allowing divesture when desired with a two-three divest year goal. There can be sheltered income options. Each associate has their personal tax plan and goals. One can build with one’s own tax protected annuity with periodical tax-deductible contributions. Up to $5M or more of acquiring an energy rehab property one potentially deducts 100% of any income, gain, depreciation recapture, investment or ordinary, personal, real estate or business asset proceeds with a 15 year loss carry forward. We include a non-disclosure confidentiality document for doing business. We are searching for long term integrity associates with common goals. Look forward to knowing you and your goals. Confidentiality-Non Disclosure Agreement PayNoTax.com – Ken Wheeler Jr. Sample Tax Scenario

Funding of property or asset (BASIS): $200,000.00

Divest or sell for: $300,000.00 Gain or Profit $100,000.00 TAXABLE $100,0000 For an energy rehab $100,000.00 is the prime amount to deduct so is the first amount to consider to transfer to the energy rehab property. One does not have to transfer the complete amount as in a 1031 qualified exchange or other defer/deduct methods. The energy rehab property is real property so when one divests one can choose any other business property to defer tax with the 1031 rule or refund into another energy rehab property with or without basis, deducting all. With the right people one can have as an energy property annuity to receive and deduct most income and proceeds from any transaction.

|

Receive PayNoTax & 1031FEC news & project updates subscribe here

Free Consultation & Discounted Experienced Local Will,Trust & Estate Advisors

Note: Your Personal or Business Tax Advisor is your final advisor for consultation. Free Consultation Appointment

1031FEC Page: (Net Investment Income Tax)

Go to PayNoTax Page4 (Sale-Leaseback)

C.P.R.E.S

|

Ken Wheeler Jr. Mobile (515) 238-9266

Business Entry-Management-Exit

Plans - BEME

Tax Reduction - Legal - Estate

- Tax

- Exit Planning

Your Own Tax Advantaged Opportunity Zone Property Manager Representative

Financial Exchange Coterie Florida International Trade Center 5206 Station Way Sarasota, FL 34233 Message Only (941) 227-3024 - Voice 800-333-0801 - Fax: 888-898-6009 www.linkedin.com/in/kenwheeler65/ Licensed Real Estate Broker Advisor Contact us for free consultation For Tax Updates and News View on Facebook @1LessTax |

|

Tax and Legal Advisors always recommended.

Thank you for visiting!

Copyright © 2018 K. B. Wheeler Jr. All rights reserved.